Portfolio Rebalancing

Recalibrate portfolios to lock in market returns and guard against risk

Market shifts happen by the second. As soon as an investment portfolio has been constructed to be optimized against specific objectives, it’s almost instantly sub-optimal.

Modern Portfolio Theory holds that it is possible to optimally allocate investments between assets to maximize expected return, based on a given level of market risk.

To empower you to do so, Quantly provides tools to monitor the performance of your investment portfolios and continually rebalance them to be best positioned to outperform the market, given a defined risk profile and other preferences.

For each of your portfolios, the Quantly platform will recommend a more optimal portfolio, using options to achieve the desired balance.

Our rebalancing algorithm constructs these efficient portfolios by examining asset correlation and using the optimization scheme you specify, including:

Markowitz: Quantly will seek to reach a specified return with minimal variance using a Markowitz mean-variance optimization; you define the frequency

Buy and hold: Quantly will maintain a static asset allocation and rely on manual rebalancing

Equal weights: Quantly will seek to maintain a static allocation of weights and will rebalance as asset prices fluctuate; you define the frequency

Use Quantly’s point-and-click interface for:

Portfolio Analysis

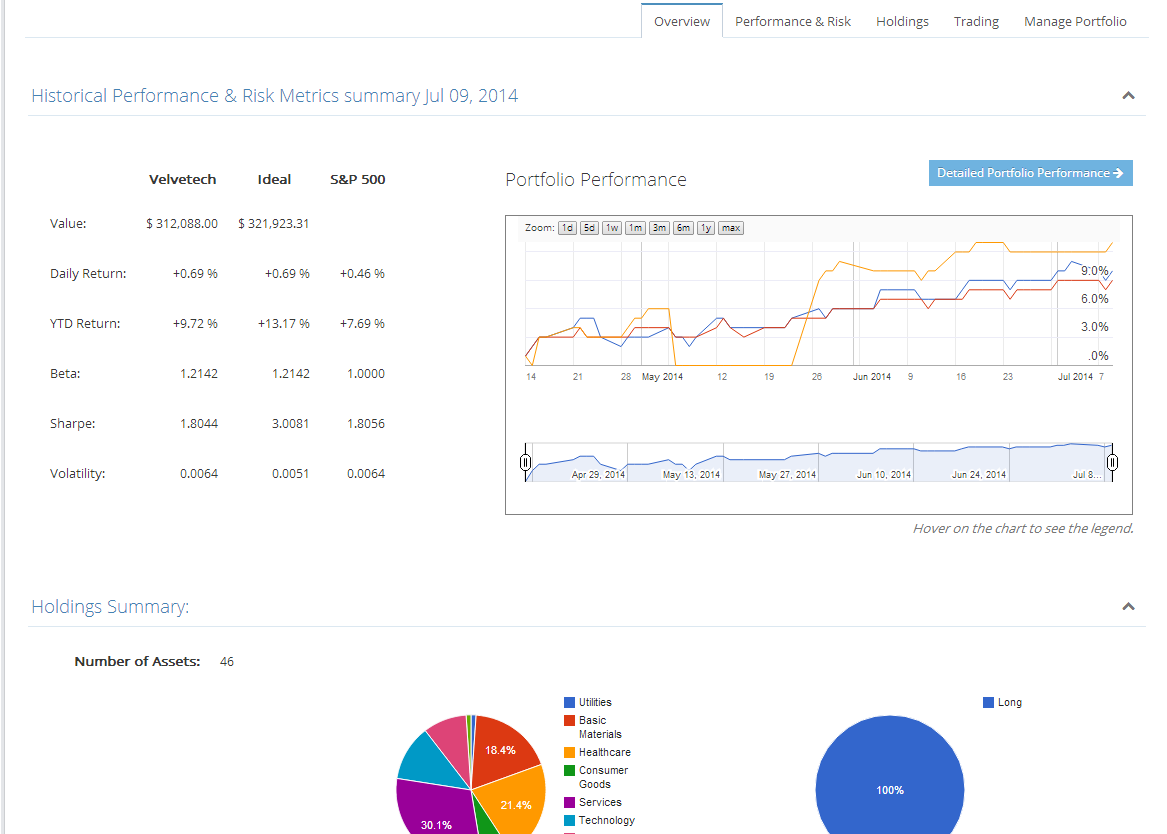

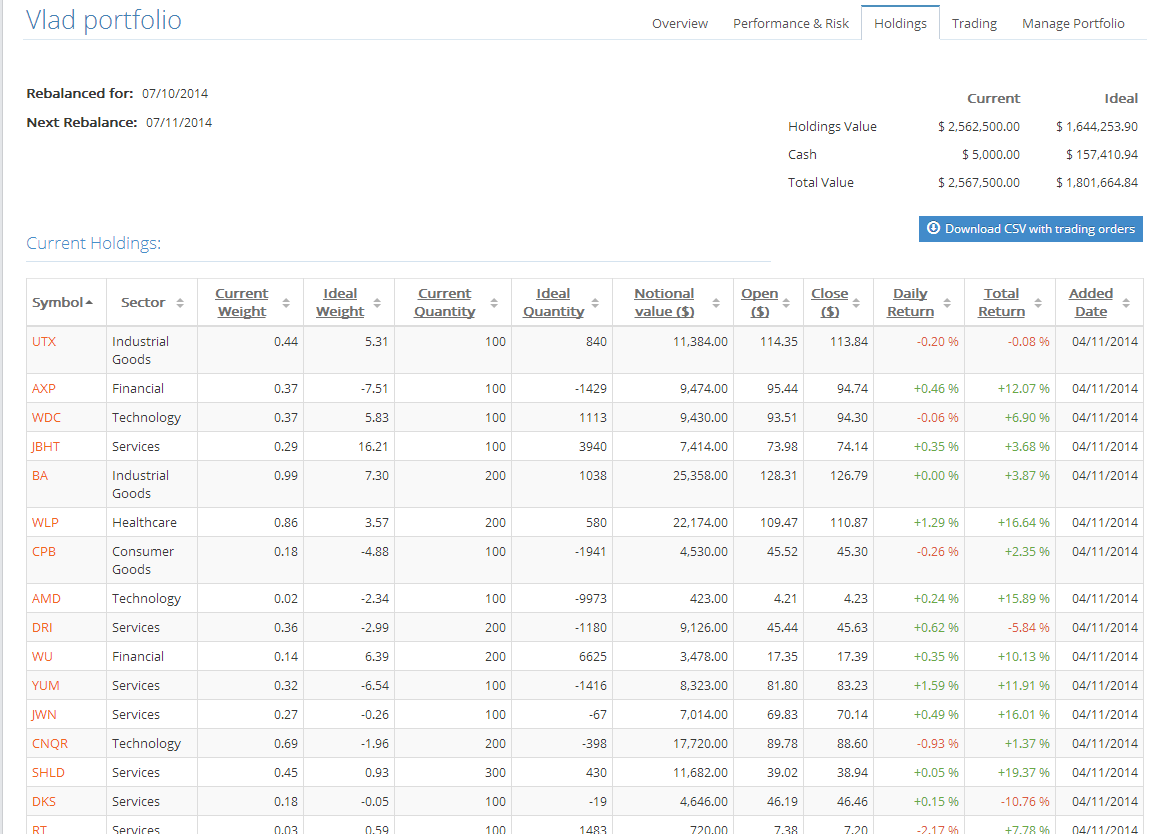

- Monitor all portfolios under your direction at a glance

- View value, year-to-date and daily return, volatility, weighting and other indicators.

- Drill into each portfolio for performance and risk metrics, holdings breakdown and more.

- Compare portfolios to market indexes.

Portfolio Optimization

- Automate or manually set rebalance schemes, frequency, desired return and use of shorts.

- Review suggested optimal portfolios and execute trades as needed.

Portfolio Management

- Portfolio Allocation and Automated Rebalancing: Derive a mean-variance optimal allocation for any provided portfolio of US Equities and ETFs, based on an asset allocation algorithm rooted in modern portfolio theory; track and further rebalance the portfolio at user-specified intervals.

- Backtesting: Backtest the performance of various portfolio allocations using our historical asset database, including the performance of the automated rebalancing engine.

- Sector Selection: Observe and optimize the portfolio's exposure to various macro sectors using our database of US Equities.

- Benchmarking and Performance Tracking: Compare portfolios against leading US indices and portfolio historical performance through built in charting and visualization or via export to Excel.

- Extendable Algorithm Platform: We can add custom asset allocation algorithms to our framework for automated asset allocation, backtesting and performance tracking alongside our native asset allocation algorithm.

- Consulting: Quantly's experts work with you to tailor the platform to your needs and the needs of your clients.

Our use of options is based on current research(1) demonstrating that rebalancing using options enables investors to systematize their portfolio rebalancing in a manner superior to calendar or trigger-based approaches, while allowing them to enhance portfolio returns and return-risk ratios.